Changes on the Way

The Tax Cuts & Job Act

On December 22, 2017 the new tax bill was signed by President Trump. There are many questions and concerns that come to mind as to what the changes consist of. Here at Whiteside and Simms we have been following the updates as they emerge, and we have laid them out here for you.

On December 22, 2017 the new tax bill was signed by President Trump. There are many questions and concerns that come to mind as to what the changes consist of. Here at Whiteside and Simms we have been following the updates as they emerge, and we have laid them out here for you.

How will this impact individual income tax?

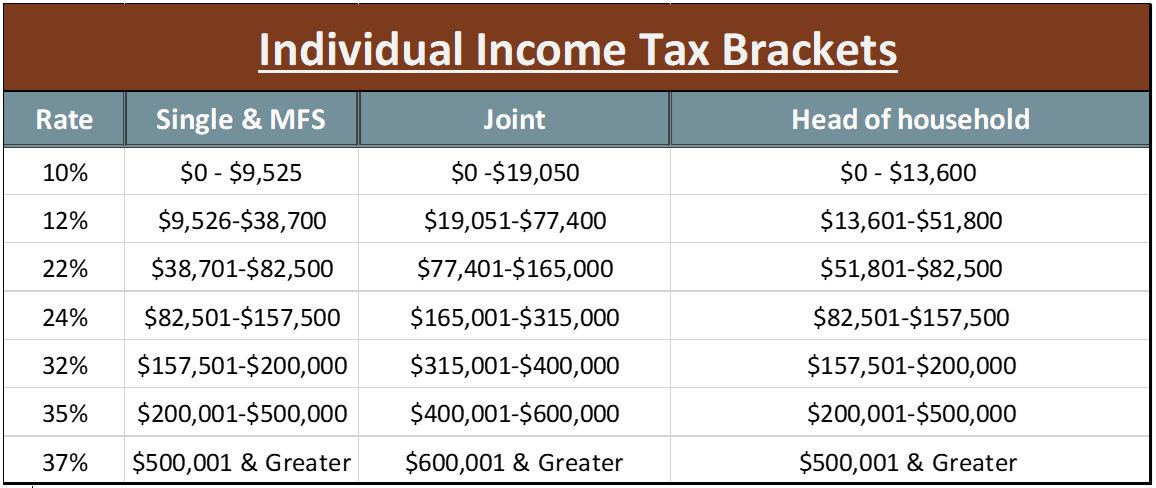

The seven tax brackets will still be implemented with some of the percentages changing.

The rates consist of 10,12,22,24,32,35, &37%. The highest rate of 37% applies to single and individuals who file married filing separately with the threshold of $500,000. For the married filing jointly taxpayers, the 37% rate will be applied to incomes exceeding $600,000.

Standard deductions & personal exemptions

It nearly doubles the standard deduction for taxpayers who are married filing jointly to $24,000, for head of household filers $18,000, and for all other individual taxpayers it will be $12,000. The additional standard deduction for the elderly and blind are still permitted. Personal exemptions are eliminated with the new tax legislation.

Family tax credits

The child tax credit will double to $2,000 per qualifying child, under the age of 17, with up to a $1,400 refundable portion. A $500 credit for other dependents will be included as one of the changes. The family tax credit phase outs will start at $200,000 for single individuals and $400,000 for couples.

Itemized deductions

State and local tax deductions will be limited to $10,000. Moving expense deductions are being eliminated except for members of the military. The medical expense deduction is being expanded for tax years 2017 & 2018 by increasing the threshold to 7.5% of your income.

The mortgage interest deductions will be limited to payments on the first $750,000 of debt owed. However, this change will not affect home acquisition mortgages made before December 16, 2017, if the home purchase closes before April 1, 2018.

Other individual taxes

The estate tax threshold has increased to estates above $11.2 million. For pass-through income there will be a 20% deduction.

AMT has been kept in place as far as individuals are concerned.

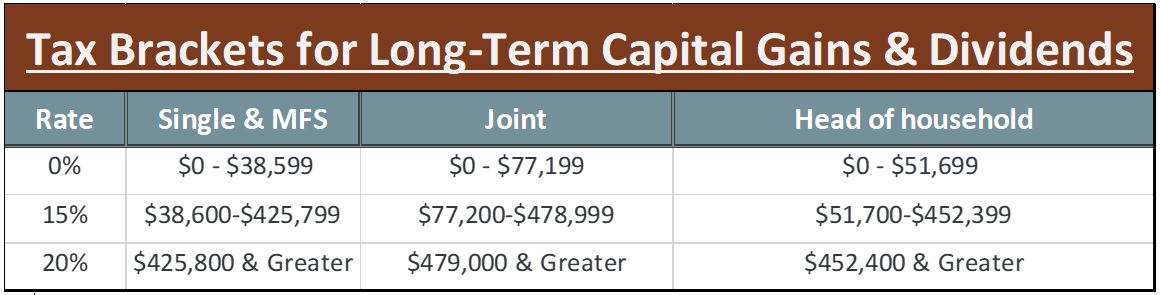

Taxation of capital gains and qualified dividends has not changed, with an exception to the income levels. For married taxpayers filing jointly a 15% rate will start at $77,200, head of household filers $51,700, and for other individuals $38,600. A 20% rate applies to married filing jointly taxpayers starting at $479,000, head of household filers $452,400, and for other individuals $425,800.

Corporations will see changes as well

The new tax bill will lower the corporate tax rate from 35% to 21%, to take into effect January 1, 2018.

The business interest deduction will be capped at 30% of income, excluding depreciation. The AMT calculation for businesses will be eliminated.

Five years of full expensing will be allowable for new investment purchases, then will phase out over five more years. Section 179 expensing will increase limitations to $1 million. The deduction for net operating losses is being limited to 80% of taxable income. As well as, research & development expenditures, they would need to be written off gradually.

Business credits

There will not be any changes to the renewable electricity tax credit nor the private activity tax exempt bonds.

Changes for 2019

In 2019, we will see the individual mandate penalty be eliminated. This will eliminate the penalty imposed on taxpayers who do not obtain health insurance. Also beginning in 2019, alimony payments will no longer be deductible if they are required by a divorce agreement after December 31,2018. Beneficiaries of nondeductible payments will not be required to include payments in their taxable income.

We will continue to monitor these changes as they are updated. If you have any questions regarding the new tax reform or any other tax matters, please contact us to schedule an appointment today.

If you would like to read more on these new tax laws, you can visit the following websites:

https://www.aicpa.org/taxreform

https://www.nytimes.com/interactive/2017/12/15/us/politics/final-republican-tax-bill-cuts.html